Yellen’s Go-To Measure Shows U.S. Debt Is Still Getting Cheaper

Yields Have a Long Way to Go Before They Sting Yellen’s Treasury

(Bloomberg) -- As rising government bond yields stir up angst on financial markets, one person who sounds unfazed is U.S. Treasury Secretary Janet Yellen. Her own go-to measure of debt costs is headed in the opposite direction.

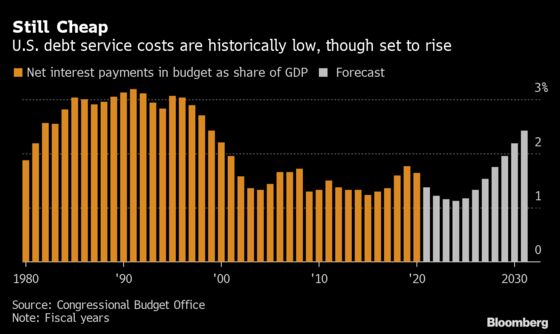

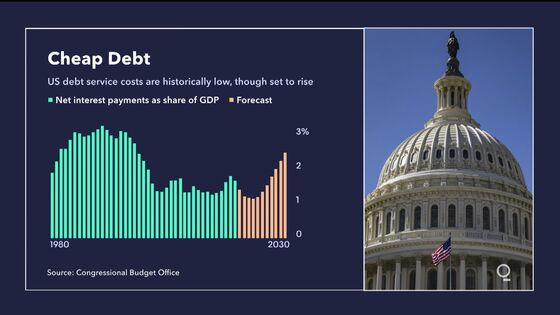

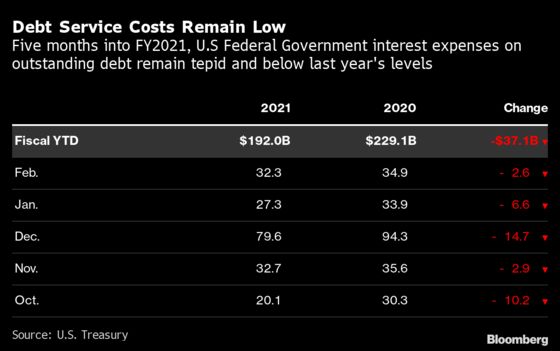

Interest payments on the national debt fell last year, to $345 billion or 1.6% of gross domestic product. They’re on track to shrink further in 2021 -- even after all the pandemic spending, plus a debt-market selloff that’s taken 10-year Treasury yields to the highest in more than 12 months.

That’s because the government is rolling over bonds it sold years or decades ago, when its borrowing costs were higher. It would take Treasury yields averaging about 2.5% across all maturities -- well above where they are now -- to turn that trend around, according to calculations by Bloomberg Intelligence. Even then, U.S. debt service costs would be comfortably lower than they’ve been in the recent past.

All of this helps explain why President Joe Biden’s administration, which just passed a $1.9 trillion pandemic relief bill, is lining up trillions of dollars more spending to help infrastructure and industry -- and isn’t concerned if it has to borrow a chunk of the money.

‘Troublesome Zone’

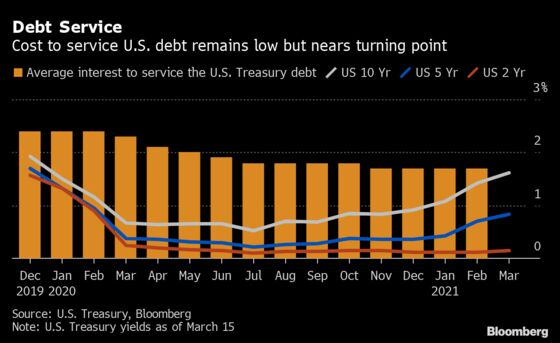

Public spending to counter the pandemic has already taken U.S. debt to a post-World War II record. And the cost of new borrowing has jumped. Ten-year yields were trading at 1.61% as of 3 p.m. on Tuesday -- double what they were as recently as November. The increase has been driven by expectations of faster growth and inflation, as vaccines enable a consumer rebound from the pandemic slump.

But Yellen says that the size of the government’s interest payments are the best guide to how much spending room there is. As a share of the economy, those outlays are “no higher than they were back in 2007,” she told ABC’s “This Week” on Sunday -- even though the national debt is more than twice as big as it was back then.

By Yellen’s preferred measure, “we are not in a troublesome zone,” said David Wessel, director of the Hutchins Center on Fiscal and Monetary Policy at the Brookings Institution.

That doesn’t mean there are no potential problems ahead.

Sooner or later, U.S. debt service costs will likely start rising again. The Congressional Budget Office doesn’t expect it to happen until 2025, after interest payments bottom out at 1.1% of GDP, the lowest since at least the early 1960s.

Historically Normal

That projection is based on the assumption of a gradual rise in 10-year Treasury rates of about 20 basis points a year, from 0.9% in 2020 to 1.5% in 2023. By contrast, in the past few weeks alone, yields have surged some 70 basis points. The CBO, which has consistently overestimated interest rates in the past decade, could be wrong in the other direction this time.

Analysts at Goldman Sachs Group Inc. predict a steeper climb in yields, with the 10-year rate ending this year at 1.9% and climbing to 2.4% in 2024. Even so, that would “leave debt-servicing costs well within the normal historical range,” Goldman economists Laura Nicolae and Ronnie Walker wrote in a March 10 report.

What Bloomberg Intelligence Says

“Debt service costs change slowly over time, and rising yields at the moment won’t significantly increase the interest taxpayers owe on current debt. However, all the new debt that is being issued will cause total financing payments to increase which over time will reduce the government’s flexibility in allocating discretionary portions of the budget. As long as the yield curve remains relatively steep and most government financing is done shorter term, interest costs shouldn’t rise much.”

-- Ira F. Jersey, chief U.S. interest-rate strategist

Still, the uncertainty over “how much is too much” when it comes to government debt is a good reason for the Biden administration to finance at least some of its forthcoming spending measures by raising revenue rather than borrowing, according to Wessel at Brookings.

“The case for building in some tax increases into the next bill, even if they don’t take effect immediately, is probably prudent,” he said. “Just to give us a little bit of comfort that we aren’t going to run up the debt too big.”

‘Great Capacity’

Last year’s budget deficit, a peacetime record at close to 16% of GDP, paid for pandemic stimulus that’s gone a long way toward reviving the economy. Biden is now juicing it some more. It’s that prospect of faster growth, and higher inflation to accompany it, that’s sent bond yields on a tear – and stung fixed-income investors. The Bloomberg Barclays U.S. Aggregate Index is down 3.4% this year.

While markets fret about inflation, officials are more focused on lingering pandemic shortfalls -– like a jobs gap of more than 9 million compared with a year ago. That’s what is driving policy.

The Federal Reserve, which starts a two-day meeting Tuesday, says it won’t raise interest rates or trim bond purchases anytime soon. Biden and Yellen say the risk of spending too little outweighs the risk of spending too much.

While the U.S. has gone further than most, similar policies have been enacted all over the world during the pandemic. Group of Seven governments borrowed a net $7 trillion in 2020. At the current low interest rates, the cost of servicing all that debt is actually negative after adjustment for inflation, according to a Bloomberg Economics analysis.

“The U.S. government continues to have great capacity to borrow,” said David Levy, chairman of Jerome Levy Forecasting Center LLC. “Market constraints on the further expansion of fiscal deficits are far more likely to show up in emerging-market countries and some others, not in the United States.”

©2021 Bloomberg L.P.