The Dollar’s Crash Is Only Just Beginning

America’s net domestic savings rate has fallen by the most on record, making the economy even more reliant on foreign money.

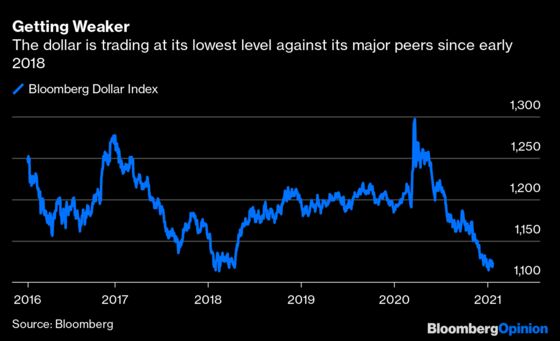

(Bloomberg Opinion) -- After an initial spike higher, the dollar has been falling steadily since the Covid-19 pandemic took hold in the U.S. last March. It is down about 10% to 12% relative to America’s major trading partners, dropping to its weakest levels since early 2018 as measured by several of the broad dollar indexes. There is more to come.

Based on a wildly unpopular forecast that I made in June of a 35% decline in the value of the dollar by the end of 2021, we are only in the third inning of a nine-inning baseball game. If that forecast comes to pass, it will provide an important exclamation point on the first year in office for America’s 46th president, Joe Biden.

There were three main reasons why I argued the dollar would fall: 1) a sharp widening in the U.S. current-account deficit, 2) the rise of the euro, and 3) a Federal Reserve that would do little in response to any weakness in the greenback. On each of these counts, I have greater conviction on the weak-dollar call today than I did six months ago. Consider the following:

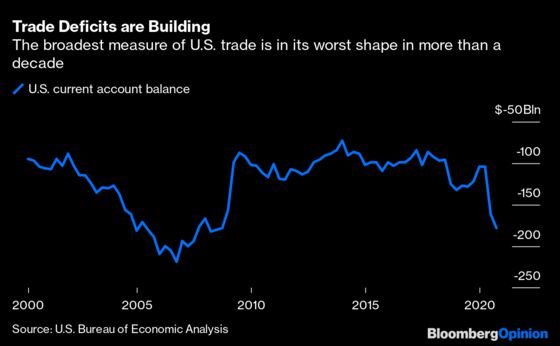

The current account. As expected, the current-account deficit (the broadest measure of trade because it includes investment income) has deteriorated further, widening by 1.2 percentage points to 3.3% of gross domestic product in the second quarter of 2020 and by an additional 0.1 percentage point to 3.4% in the third quarter. The shift in the second quarter was the largest erosion on record, and at its current level the deficit is at its worst since the end of 2008.

At work is a deterioration in domestic saving driven by explosive Covid-related increases in the federal budget deficit. When a nation is lacking in saving and wants to invest and grow, it must import surplus saving from abroad to square the circle, running current-account deficits in order to attract the foreign capital.

Unsurprisingly, the identities have held. The net domestic saving rate (depreciation-adjusted saving of businesses, individuals and the government sector, combined) fell below zero in the second and third quarters for the first time in a decade. The 3.8-percentage-point decline in the net domestic rate to negative 0.9% in the second quarter from a positive 2.9% rate in the first quarter was also the largest quarterly decline on record.

The second-quarter plunge in domestic saving was largely an outgrowth of the $2.2 trillion Cares Act, which was aimed at providing fiscal relief during the Covid-related lockdown. With the pandemic and its aftershocks still very much in evidence, another $2.8 trillion of fiscal relief is in the offing — $900 billion already signed into law in December 2020 and another $1.9 trillion proposed by Biden.

The combined Covid relief packages total $5 trillion, or 24% of 2020 GDP. While not stimulus in the conventional sense, this fiscal injection breaks all modern records by a wide margin. The domestic saving rate, as a result, should plunge further below zero, putting the already wide current-account deficit under even more intense downward pressure. Although the international imbalance may not break the prior record of minus 6.3% hit in late 2005 as I argued in June, it is likely to come close.

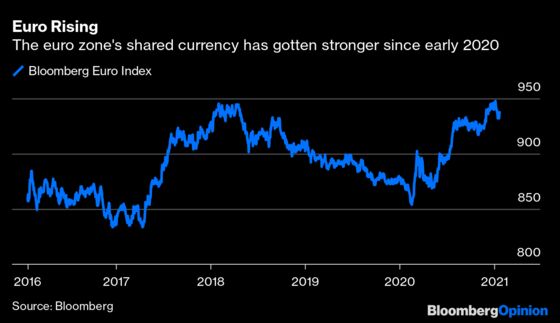

The euro. The pushback on my negative dollar call was all about TINA — There Is No Alternative. In a follow-up commentary, I countered that claim, attempting to make the positive case for the Chinese renminbi and the euro, while also giving a nod to precious metals and even crypto currencies.

Although China’s yuan has appreciated about 4% since last June and should continue to strengthen as China leads the post-Covid global recovery, the euro has moved little over that same period (after rising about 7% from February to May). As a congenital euro-skeptic, I have always had a hard time saying anything terribly constructive about the shared currency. That’s because the currency union had a critical flaw: a single currency and central bank but no unified fiscal policy.

The surprise came in July when German Chancellor Angela Merkel and French President Emanuel Macron reached agreement on a relief package that featured a pan-regional fiscal backstop in the 750 billion euro ($908 billion) Next Generation EU fund, complete with sovereign bond issuing authority. This adds the missing fiscal piece to the currency union, quite possibly providing a “Hamiltonian moment” for the most undervalued major currency in the world.

Meanwhile, gold prices surged for a couple of months in June and July but then retraced those gains over the balance of the year. It was a different story for cryptocurrencies. Little did I know what was to come for Bitcoin, which surged four-fold since June, or two-and-a-half times the late 2017 spike that, at the time, had been depicted as one of the greatest speculative bubbles in history.

The Federal Reserve. When current-account deficits are under pressure, the central bank can usually be counted on to come to the rescue by tightening monetary policy. That, most assuredly, is not the case with today’s Fed. By adopting a new “average inflation” targeting regime in August, the Fed has sent a strong signal that it will move later rather than sooner to counter any surge in inflation rates.

Nor can so-called Modern Monetary Theory ride to the rescue of the dollar. Yes, debt and deficits may not be consequential in a low inflation, low interest rate climate — hardly a brilliant theoretical breakthrough — but saving, or the lack thereof, still matters. With the U.S. increasingly reliant on foreign capital to compensate for its growing shortfall of domestic saving and with the Fed’s open-ended quantitative easing measures creating a massive overhang of excess liquidity, the case for a sharp further weakening of the dollar looks more compelling than ever.

A still-raging pandemic and an economy on the brink of a double-dip recession leaves the Biden administration with no choice other than to opt for another round of massive fiscal relief. This outcome would have consequences for any economy. For saving-short America, it spells a weaker dollar.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Roach, a faculty member at Yale University and former chairman of Morgan Stanley Asia, is the author of "Unbalanced: The Codependency of America and China."

©2021 Bloomberg L.P.