(Bloomberg Opinion) -- This is a big year for the U.S. oil and gas industry. If the past five have constituted a reckoning with the old frack-it-till-you-make-it model, then this one is where we find out if the reckoning stuck.

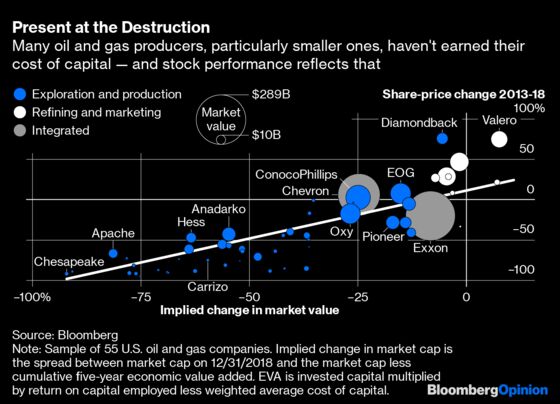

The new mantra espoused by many energy companies is that returns are king. They are. The chart below, which I have adapted from one used by Kimmeridge Energy Management Co., shows the close relationship between return on capital and stock performance. It compares how share prices moved in the five years through the end of 2018 with an implied change in the market cap based on that period’s cumulative economic value added, a measure of value creation or destruction. The sample consists of 55 U.S. oil and gas companies with a market cap of at least $250 million (as it runs through the end of 2018, it includes a couple of companies acquired since then, Anadarko Petroleum Corp. and Carrizo Oil & Gas Inc.).

More pertinent is that bigger companies — especially refiners — tended to fare better than the cloud of smaller bubbles trailing off to the bottom left of that chart. This gets at a critical issue regarding what comes next for the sector.

The past decade’s boom in U.S. oil and gas production owed much to a crowd of relatively small companies competing with each other and backed by enthusiastic capital markets. But as oil has settled into a lower, more volatile range (and gas has fallen into a coma), so the advantages of being bigger have become apparent. Smaller exploration and production companies, in particular, tend to have higher unit costs and lower valuation multiples (i.e., a higher cost of capital; see this).

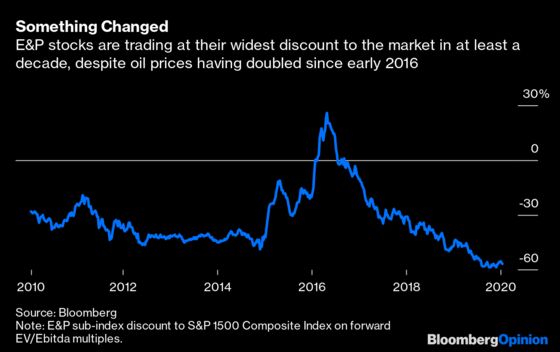

The sector has been structurally devalued versus the wider stock market. Moreover, while average yields on energy junk bonds have come in from December’s peak of almost 10%, they remain above 8%, markedly higher than the 5-7% range that held through much of the past decade.

Higher risk premiums mean a higher hurdle to beat than the one the sector largely missed already over the past five years or so. Notwithstanding President Donald Trump’s efforts to reduce regulatory costs, climate concerns are likely to widen those risk premiums further over time.

That was the message in BlackRock Inc. CEO Larry Fink’s latest missive on the subject. As I wrote here, even if most of the money BlackRock manages is passive, it can still use that to vote for change in the governance standards prevalent in the sector that have prioritized growth above all and protected incumbent management teams. And based on data compiled by Bloomberg, BlackRock holds roughly $25 billion worth across more than 100 U.S. E&P firms, adding up to an average stake of 7% (albeit ranging from virtually zero for some stocks all the way up to 15%).

With capital costlier than it used to be, the imperative for smaller companies in particular to consolidate and jettison the cost burden that comes with maintaining separate identities (and management and campuses and accounting and ...) is getting ever stronger. Two decades ago, the supermajors were created in response to a structural change in the investment landscape for oil and gas. We are at that point again, only at the opposite end of the scale.

-- With assistance from Elaine He and Denise Cochran

Economic value added values are pulled from the Bloomberg Terminal. They are calculated by multiplying invested capital by the spread between return on capital employed and weighted average cost of capital, with a positive value indicating value creation and negative indicating destruction. I then compare the cumulative figure with each company's market cap at the end of 2018 to get an implied percentage of value that was either created or destroyed. Data run for the five years through 2018 as that is the last year of complete annual economic value added figures.

The correlation coefficient is 0.74; coefficient of determination is 0.55.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.