(Bloomberg Opinion) -- Rapidly rising housing prices in the U.S. has led to talk of another housing bubble like the one that helped trigger the financial crisis a little more than a decade ago. Consider that the Case-Shiller National Home Price index has gained in excess of 6% per year on average since January 2012, while net rental income has barely kept up with inflation, increasing just less than 2% per year. The result is that home prices seem as overvalued as they were in the spring of 2005, nine months before the peak.

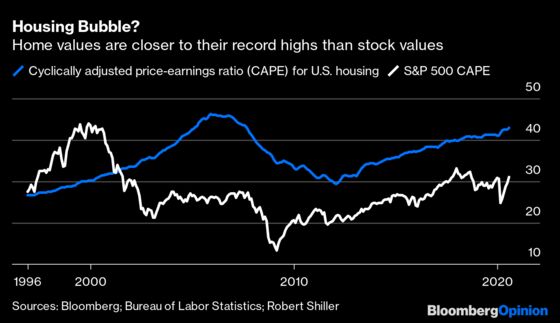

One way to measure home valuations is with a cyclically adjusted price to earnings (CAPE) ratio developed by Yale University professor and Nobel Laureate Robert Shiller for stocks. The concept can be applied to a broad swath of assets by dividing the current price of an asset by the average annual inflation-adjusted earnings over the prior 10 years. The chart below shows CAPE for U.S. home prices and the S&P 500 Index since 1996.

Stock valuations soared in the late 1990s, only to crash from 2000 – 2002, tread water for six years, then tumble again in 2008. Home valuations ignored the 2000 equity crash, but shared the 2008 crash. Since then the two have increased roughly in line, but with home prices starting from a higher level. As a result, equity valuations are still well below peak values, but home prices are approaching the historic highs.

Much of the focus on the housing market lately has centered on the short-term environment, with the low inventory of homes cited for rising prices and a jump in rental vacancy rates driving rents lower. But if the concern is the possibility of major economic disruption—rather than just whether houses are good investments at current prices— the focus should be on long-term macroeconomics. Sure, real estate prices always drift up or down, and differ by location and type of home. A bubble in housing requires widespread overvaluation over years, which is what we have witnessed.

Home valuations are worrisome, but for different reasons than 2006. One minor point of comfort is the run-up from 1996 – 2006 displayed a classic bubble pattern of accelerating price increases near the peak. The increase in valuations since 2012 has been linear, with no sign of steepening.

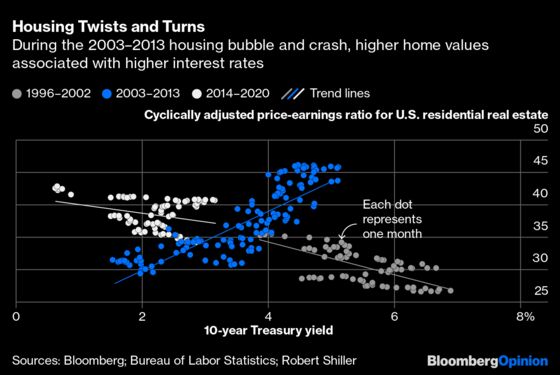

A bigger difference is illustrated in the chart below, showing the CAPE ratio for housing versus 10-year U.S. Treasury note yields (these correlate with mortgage rates, but are a better predictor of home prices statistically). In both 1996 – 2002 (grey dots) and 2014 – 2020 (white dots) home values linearly decreased with interest rates, at about an 8% decline in valuations for every 100 basis-point increase in yields. This is in line with longer history. But during the 2003 – 2013 bubble and crash (blue dots), there was a much steeper relation in the opposite direction—higher home values associated with higher yields.

The reason for the reversal during the housing bubble was capital rushing into mortgages via structured investment products, insulating home buyers from paying higher rates. More than half of new mortgages were adjustable with low teaser rates divorced from economic reality. Today, less than 10% of new mortgages have adjustable rates, according to data from Freddie Mac. In 2005, investors were pushing mortgage originators to prod home buyers into paying higher prices by providing them with easy access to funds. This was not a price increase driven by demand for housing. The bubble popped for financial reasons, not housing reasons, and—unlike previous waves of mortgage defaults—it brought much of the financial system down with it.

Today’s high valuations can be explained by low interest rates, as has been the usual pattern in the past. That might lead one to expect a typical correction, where housing prices deflate over a few years with differences among regions. Many homeowners are hurt in places where prices were especially high, and also in places with especially bad economic problems, but nationally diversified mortgage securities follow historic trends and financial institutions deal with losses seamlessly. Homeowners who can wait out the decline will see valuations increase above their purchase prices in five years or so.

The bad news is all previous history came at higher mortgage rates. The average 30-year fixed mortgage rate fell below 3% for the first time in August 2020, and rates are close to the lowest possible levels given the credit risk and costs of writing mortgages. It’s one thing to be a peak valuation, it’s another to be at peak valuation with no discernable upside.

It’s implausible that housing prices can go up from here without large increases in rents, which require increases in demand for housing. That’s an unlikely outcome in a recession. If the recession continues, where will new demand come from? If it ends, interest rates go up, pushing housing prices down.

The good news is this is not a disaster market. There’s no evidence home price declines could threaten the financial system, nor create mass economic distress as we saw after 2007. No doubt there remain plenty of bargains in regions with robust economies where prices have not overheated. The bad news is there’s a lot more downside than upside for average homebuyers, and some of them are very likely to suffer in 2021.

One interpretation of CAPE is how many years it takes to earn your purchase price back, adjusted for inflation, assuming earnings increase with inflation.

Earnings for public companies come from their financial reports. “Earnings” for home buying consist of the net rental income—rent minus expenses—received by a landlord or the monthly savings of a homeowner relative to a renter. In the latter case we include expenses like property taxes, maintenance and insurance, but not mortgage payments, which are a financing cost. The home price CAPEs given here are my calculations from Consumer Expenditure Surveys and Bureau of Labor Statistics reports.

One caution is the S&P500 CAPE is based on clear published values, but “earnings” from home ownership have to be estimated from survey data. Everyone agrees on the S&P500 CAPE, but different analysts come up with different CAPEs for housing. Nevertheless, I think the relative values are reliable—the home price CAPEs might be over or underestimated relative to stocks, but the 2020 values should be consistent with the 2006 values. Another caution is that real estate data is smoothed and lagged. If we better home price and cost data, the housing CAPE would look more jagged like the S&P 500 CAPE.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Aaron Brown is a former managing director and head of financial market research at AQR Capital Management. He is the author of "The Poker Face of Wall Street." He may have a stake in the areas he writes about.

©2020 Bloomberg L.P.