Flood of Cash With Indian Banks May Prompt RBI to Use New Tool

The Reserve Bank of India is running out of bonds to lend out.

(Bloomberg) -- The Reserve Bank of India is running out of bonds to lend out.

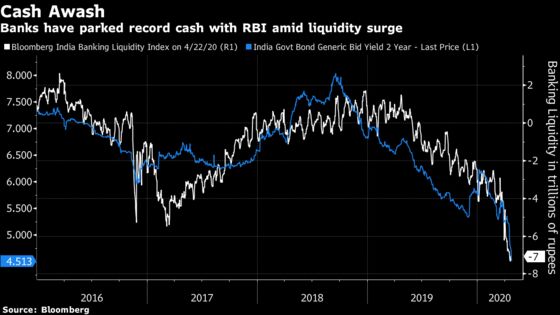

With the nation on lockdown, banks have parked an average of 7 trillion rupees ($92 billion) overnight with the RBI in the past week in return for bonds. That’s more than 70% of the securities held on the central bank’s books, according to the latest data.

The depletion has sparked talks about the RBI deploying the so-called Standing Deposit Facility, which will enable it to take in the money at a cheaper rate without offering collateral. The central bank was pushed closer to a similar situation in the aftermath of Prime Minister Narendra Modi’s shock cash ban on high-value currency in 2016 that left the banking system awash with cash.

“The securities that the RBI can offer as collateral are shrinking,” said Soumyajit Niyogi, associate director at India Ratings & Research Pvt. “They’ll have no option but to resort to SDF if this liquidity overhang continues.”

Surplus banking liquidity is set to surge to 9 trillion rupees by July, as per Bloomberg Economics’ estimates. Slow credit offtake, the government borrowing more from the central bank to meet its short-term cash needs and a surge in deposit growth is adding to the liquidity. A spokesman for the central bank didn’t immediately respond to an email seeking comments.

Some analysts say the use of the SDF tool may be prompted by the desire to push the overnight rate even lower, rather than by a likely shortage of bonds. RBI can also reuse the bonds given as collateral by banks for getting funds under the long term repurchase operations, according to ICICI Securities Primary Dealership Ltd.

“Under the collateral fig leaf, the real reason behind the SDF proposal is to push down the overnight rate without the inconvenience of the monetary policy panel voting,” said A. Prasanna, chief economist at the bond underwriter. “This will also put more pressure on banks and other investors to reach for yield -- take more duration and credit risk.”

The RBI’s rate-setting panel only sets the main repurchase rate, but the central bank can tinker with the other rates and reserve ratios. Earlier this month, the authority cut the reverse-repo rate to discourage banks to park cash with it. Back in 2007, it capped bids under reverse repo to push banks into lending.

Still, risk-taking is not going to increase in the present environment and the liquidity overhang will remain, said Arvind Chari, head of fixed income at Quantum Advisors Pvt.

“SDF is coming. It is a matter of time,” he said.

©2020 Bloomberg L.P.