Berkshire’s Buffett Show Makes Way for the Next Act

The successors-in-waiting get to take the spotlight at a meeting that broke with tradition in meaningful, if subtle, ways.

(Bloomberg Opinion) -- Berkshire Hathaway Inc.’s annual shareholder meeting has come around again, and this year, it broke with tradition in some meaningful, if subtle, ways.

Warren Buffett, the longtime CEO and master of ceremonies, found himself defending the company’s commitment to value investing, amid news that one of his lieutenants recently decided to purchase Amazon.com Inc. shares. Stock buybacks were a hotter topic than the search for Buffett’s next “elephant.” And Buffett even shared the spotlight — literally — with his potential successors. First, he ceded the microphone to Ajit Jain, vice chairman of the company’s insurance operations, when a question was directed to Jain and Buffett about the riskiest types of insurance contracts.

“Ajit, why don’t you answer first, if you’d like to,” Buffett said. It was perhaps the defining moment of the event, drawing applause from around the Omaha arena — an audience of tens of thousands of investors and fans who traveled from all over the world to absorb the wisdom of the Oracle and his partner, Charlie Munger. Buffett later let Greg Abel — Berkshire’s vice chairman of non-insurance operations — take a turn at answering a question about the outlook for electricity demand and the spending needs of Berkshire Hathaway Energy, which Abel also helms. That opened the door for the two deputies to enter the conversation.

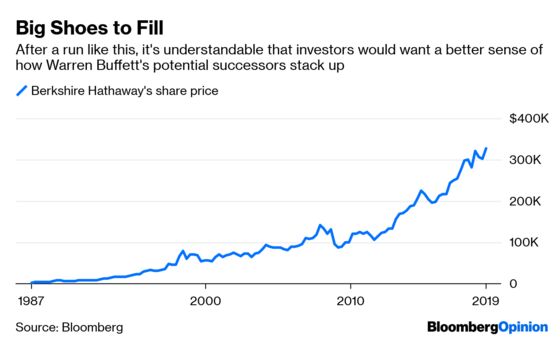

In the days leading up to the meeting, shareholders — both large and small — told me that they hoped to hear more from Abel and Jain, the men being prepped to someday run Berkshire, a conglomerate valued at $537 billion. After all, Buffett will turn 89 in August, and Munger is now 95 years old.

“Every year we think this is the last year,” said David Marcus, CEO of Summit, New Jersey-based Evermore Global Advisors, who oversees about $1 billion of assets and attended his first Berkshire meeting 20 years ago. That line of thinking partly explains the surge in attendees in recent years. “It would be nice to slowly get exposed a little more to who they are,” he said, referring to Buffett’s successor candidates.

For example, during the six-hour Q&A session, Buffett and Munger were asked about 5G data networks and also precision-scheduled railroad strategies, topics better suited for specific business heads. Buffett said as much: “We have people in those businesses who know a lot more about them than we do.”

One shareholder did ask whether Buffett would consider having Jain and Abel join him and Munger actually on stage to field questions. It’s something I’ve long wondered, too, and have argued is a necessary move to make for an easier transition when Buffett’s no longer around. Buffett’s answer was as surprising as it was refreshing, since he hasn’t typically wanted to share the limelight: “That’s probably a pretty good idea.”

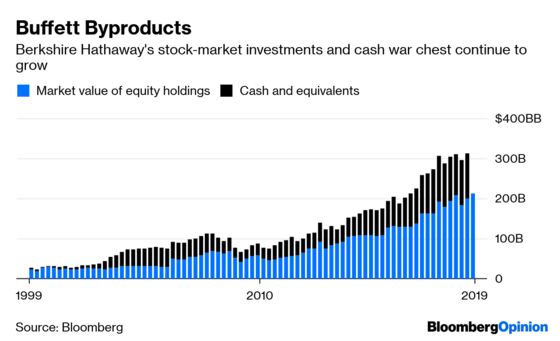

That said, Berkshire’s operations are well-run. They generated $5.56 billion of earnings in the first quarter, during which time the company’s cash pile swelled to $114 billion. So when Buffett is no longer there, the concern won’t be as much about operational strength and cultural continuity; instead, the biggest unknown is capital allocation.

The foundation of Berkshire’s success is that its entities generate enormous amounts of cash, which Buffett then uses to make high-return investments, whether in the form of corporate takeovers, stock-market purchases or, recently, buying back Berkshire’s own stock. (It spent $1.7 billion on repurchases last quarter.) That means there are more questions for Todd Combs and Ted Weschler, the stock pickers working under Buffett, than for Abel and Jain.

“Buffett and Munger are the smartest, most level-headed business people of all time, and we owe them a debt of gratitude,” said Bill Smead, CEO of Smead Capital Management, which has owned Berkshire since the early 1990s. “Our biggest disappointment is that we haven’t been allowed to understand the discipline being exercised by Todd and Ted. I’m a partner of this business, and I want to know who they are and what their thinking is.”

One of them — Buffett wouldn’t say whether it was Combs or Weschler — was behind Berkshire’s purchase of a stake in Amazon, a technology stock valued at a bold 48 times earnings. Buffett explained that he won’t give them the microphone because Berkshire’s investing calls are proprietary and it’s not an adviser, which feels like an excuse. However, his defense of the Amazon bet may resonate with investors. He said whoever was behind it is “as much a value investor” as he is, and just as Buffett will only invest in areas he grasps, this person feels they really understand Amazon. Combs and Weschler are exposing Berkshire to industries that it’s feared for lack of understanding, but shouldn’t necessarily avoid.

Plus, Berkshire needs help spending all that cash somehow. I’ve written before that if the cash keeps building and stays at unproductive levels, it may become a burden for the next CEO. And remember, the board may not feel so much loyalty to the next in line should he not live up to expectations. However, that cash cushion could also provide Buffett’s successor the necessary firepower to go full steam ahead on share buybacks when Buffett is gone and the share price undoubtedly drops. That doesn’t preclude one last megadeal from Buffett — Berkshire’s subsidiaries generated about $4 million of cash per hour last year, faster than he can keep up with.

The rest of the meeting was par for the course, with more questions this year regarding Kraft Heinz Co. As Kraft Heinz’s business took a bit of a sour turn this year, Buffett has faced criticism for his unwavering support of 3G Capital, the private equity firm driving the foodmaker’s strategy. Buffett said the business is still doing fine operationally, but that Berkshire overpaid for the merger of Kraft and Heinz in 2015 (not the initial buyout of Heinz two years earlier). “It’s not a tragedy that out of two transactions, one worked wonderfully and the other didn’t work so well,” Munger said. “That happens.”

Next year’s meeting may herald the biggest change after this year’s baby steps toward giving Abel and Jain a higher profile deserved of two people running more than five dozen businesses that span insurance, energy, transportation, retail and even candy (See’s was clearly the most popular booth at the event).

That said, people travel to Omaha mainly to hear from Buffett, said Mario Gabelli, who oversees more than $30 billion, including Berkshire class A shares, as CEO of Gamco Investors Inc. “This is the Warren show,” he said.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.